Introduction to Economics Situation of scarcity is one in which goods are limited relative to desire. Simply not enough goods and services to satisfy even a small fraction of everyone’s consumption desires. Economy must make the best use of its limited resources.

Microeconomics - Adam Smith

Behaviour of individual entities

1. Markets

2. Firms

3. House holds Macroeconomics - John Maynard Keynes (invented in 1935) - concerned with the overall performance of the economy.

Unemployment insurance - when it covers too much people start depending on the government and stop looking for work.

Balance between the discipline of the market and the compassion of government social programs.

- Consumption goods Investment goods Economics.

- Accounting, Marketing, Finance, Banking, FDI (Foreign Direct Investment)

- Science Corporations (firms)

Nash equilibrium p 214-215. Is when two firms both use the same strategy and both reach equilibrium. (also known as non cooperative equilibrium), each party has chosen the strategy best for itself – without consulting or cooperating and without regard for welfare of society or any other party.

B) The Natural resources will be managed better when technology improves. Technology allows the more efficient use of resources. Fewer resources will produce more goods as a result. This will mean that the PPF frontier will move to the right as scarce resources become utilized better to produce goods & services.

C) As time passes we learn to use resources more efficiently. But as time passes we have used up more of these resources and hence the resources become scarcer. Production becomes inefficient when it is possible to reallocate resources as a result, produce more of at least one good without producing less of any other good. As a result the production possibility curve will take longer to decrease but still decrease over a period of time. Oil is a non renewable resource, given the amount of time, millions of years it takes to regenerate. This means that it is inevitable that petroleum is going to run out as oil is required to produce this good.

3)

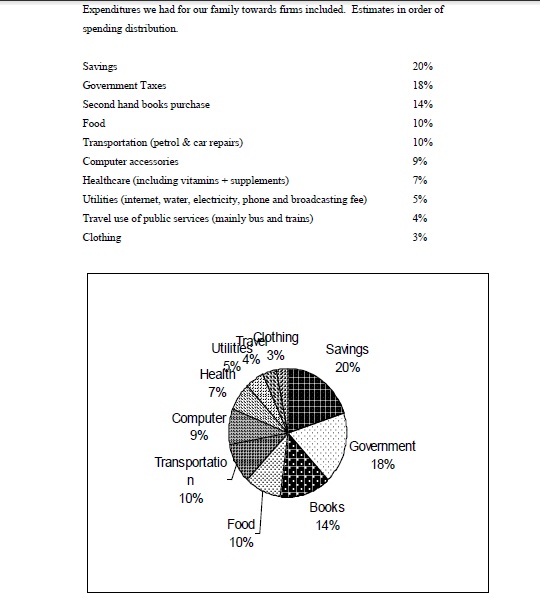

My house hold includes my dad, my brother and I. Not much came from the sale of factor services to firms as my dad is retired and self employed. I was working part time and a lot of that time was receiving a government beneficiary or student allowance subsidy. My brother was still studying in high school. I would estimate that about 90% of the income came from my dads business, which was because my dad was self employed. This means he was selling his services to his own business. The rest of the household income came from my work & income benefit or when I was working part time, or my student allowance. It is actually difficult to estimate how much household income came from my dad on a weekly basis as he sells books over the internet and in a shop, and his sales vary depending on levels of supply and demand. Which constantly swing up and down like a yo yo in the book business. It would be fair enough to say that his income was a lot higher than mine.

4)

Laissez faire is a French word which in English means leaves things alone. It implies that government should allow firms to have more say, in how they run their businesses and intervene as little as possible.

An advantage of Laissez faire is that businesses are not restricted by policies made by governments. Policies which are good for the environment such as regulating the amount of carbon that factories produce is good for the environment but costly for firms. As a result since they have to spend more on cost of production they have to put prices up to meet these new expenditures, which is also bad for the consumer. As the firms have to increase price to meet these new expenditures. A disadvantage of Laissez faire is that governments cannot intervene and influence & regulate prices. This is not good for the consumers who can benefit from lower prices and it could make items less realistically affordable

b)

Since cost of production effects supply and cotton is a production input. Equilibrium price will fall as suppliers will be able to supply the same at a lower price or more at the same price. Since the cost of raw materials for t-shirts is cheaper, more can now be produced and then supplied at the same price as well this means quantity supplied increases.

c)

The demand for t-shirts will increase as it is seen as a better substitute product/commodity. This means consumers will be prepared to pay more for t-shirts, equilibrium price will rise. Equilibrium quantity will also rise as suppliers will have more of an incentive for producing t-shirts as the market demand has rose. And the allocation resource in the market has changed.

6b.

Price is one mechanism which is used to control surpluses in a free market. Price can be decreased to increase demand so it meets better with supply at equilibrium point. Equilibrium is optimal selling in a market. That its why some firms clear stock which is not selling very well with discount sales, closing down sales & percentage reductions e.g. 25% off. The Warehouse in New Zealand is a good example of a company that frequently practices this.

Comments

Post a Comment